The critical relationship between energy security and growth: A comparison between India, China and the rest of the world

Pratim Ranjan Bose

Post On > Apr 5 2022 1280

Access to energy is a precondition of development. Naturally, a spike in energy prices impacts global growth. However, the impact of the latest rally should be particularly harsh, as the share of imports in global energy use has gone up dramatically after 2014. The weak post-pandemic fundamentals will intensify the pain.

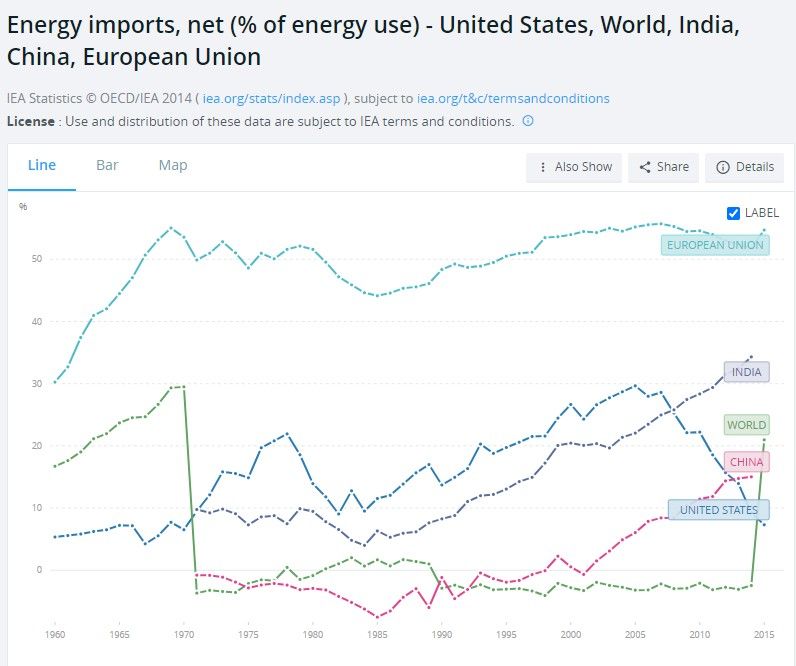

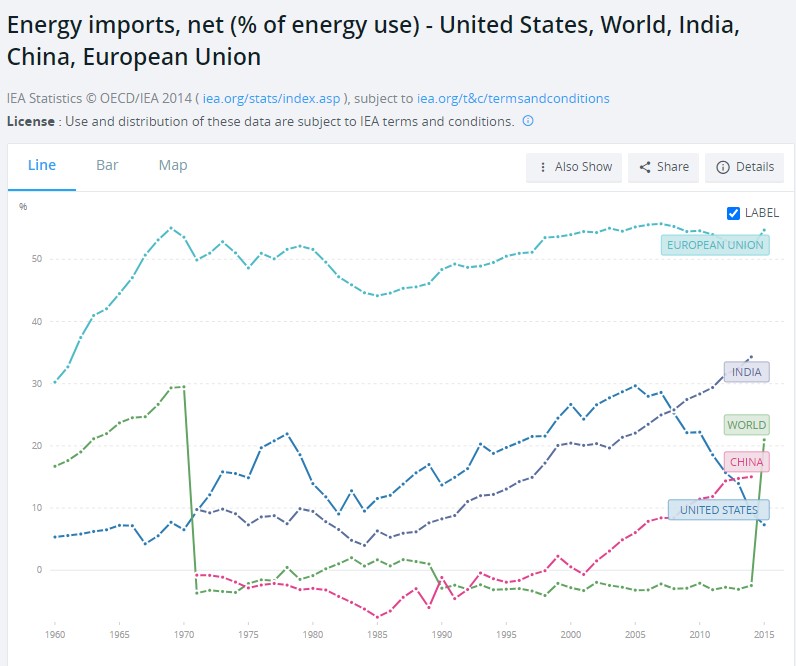

According to World Bank, the global economy was largely self-sufficient in energy between 1971 and 2014 (Figure-1). However, the share of imports (net) jumped to nearly 21% in 2015. This is a consolidated trend and experiences vary from country to country.

In 1970, the USA was largely a coal country and met barely 6-7% of its net energy use through imports. Over the next three decades, the balance tilted in favour of imports. Between 1984 and 2005, the share of imports rose three times from 10% to 30%. Interestingly, during the period the US also witnessed a decline in manufacturing activities.

Fig-1: Share of imports in energy use

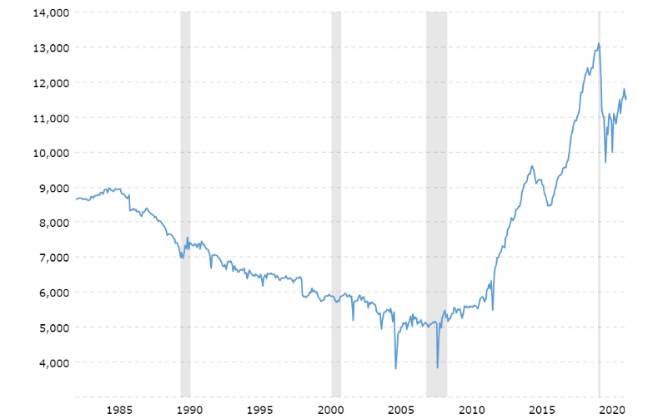

The energy use pattern changed thereafter. The US oil production trebled since 2005 (Fig-2). Shale oil was a changemaker. As of 2015, the share of net imports in total primary energy consumption was down to the level of 1970. The US recently started exporting oil.

If this has given the Joe Biden administration an extra edge in imposing sanctions on oil and gas exporting nations; Europe suffered the most from it due to high import dependency. Between 1960 and 2015, the share of imported energy increased from 30% to 55% in European Union.

Among the positives, Europe’s import curve remained flat over the last decade, arguably due to fast growth in renewables, namely solar and wind.

Fig-2: US crude oil production

The 1980s and 1990s were decades of dramatic transition in the world economy. Alongside the collapse of the Soviet Union and end of the cold war era; a whole set of nations from the less-developed South started turning the wheels of their economies at a faster rate than ever.

At the forefront of this change was China. At the stewardship of Deng Xiaoping, Beijing adopted the “Open Door” policy (Fig-3) to private and foreign capital in 1978, exactly a decade ahead of the fall of the Berlin Wall.

Over the next two decades, the socialistic economy built on the principles of self-sufficiency was converted into a global powerhouse of manufacturing and exports.

Fig-3: China’s open door policy

Normalization of the US-China relationship, opening SEZs (special economic zone) and granting special status to the Hainan province to attract foreign investments were some of the early initiatives. Energy security was a centrepiece of the policy. Coal mining was liberalised in 1978.

Over the next two decades, China reported sustained high growth. Excepting three years (1981, 1989 and 1990) growth was mostly above 8%. For two years, the economy grew at 15%.

High growth required higher energy use. However, for the majority of the two decades, China was self-sufficient in energy. According to World Bank, China had an import content in net energy use for the first time in 1999 (Fig-1). As of 2014, the import content rose to 15%, less than the global average of 21%.

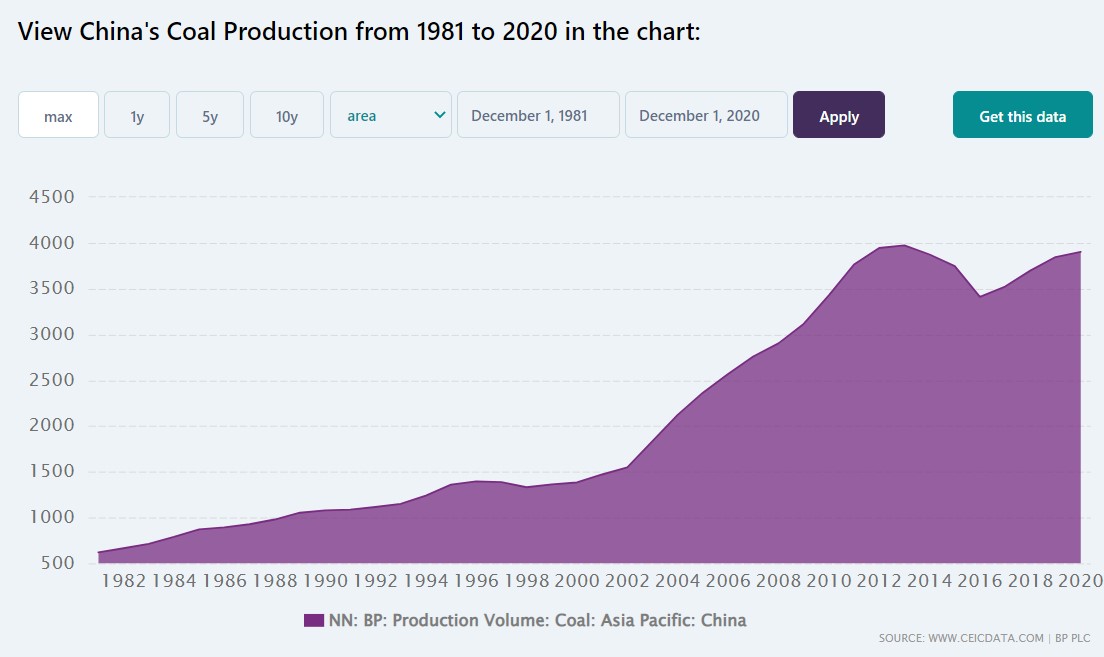

Fig-4: Coal production in China

Evidently, it was coal (Figure-4) that converted China into a global manufacturing hub. From 678 million tonne in 1978, coal production increased by 2.7 times to 1830 million tonne in 2003, energy commodity prices started firming up globally. From third (after the USA and Soviets) in global coal production in 1978, China quickly became the topmost producer.

A country cannot run on only one primary energy option. Moreover, not many countries are as resource-rich as China. However, many such countries spreading across South and South East Asia improved their growth rate during the period.

This was possible due to stable global energy commodity prices. The fast expansion of the natural gas market took away much of the steam from coal during that period. Europe started shifting away from coal with the arrival of Russian gas.

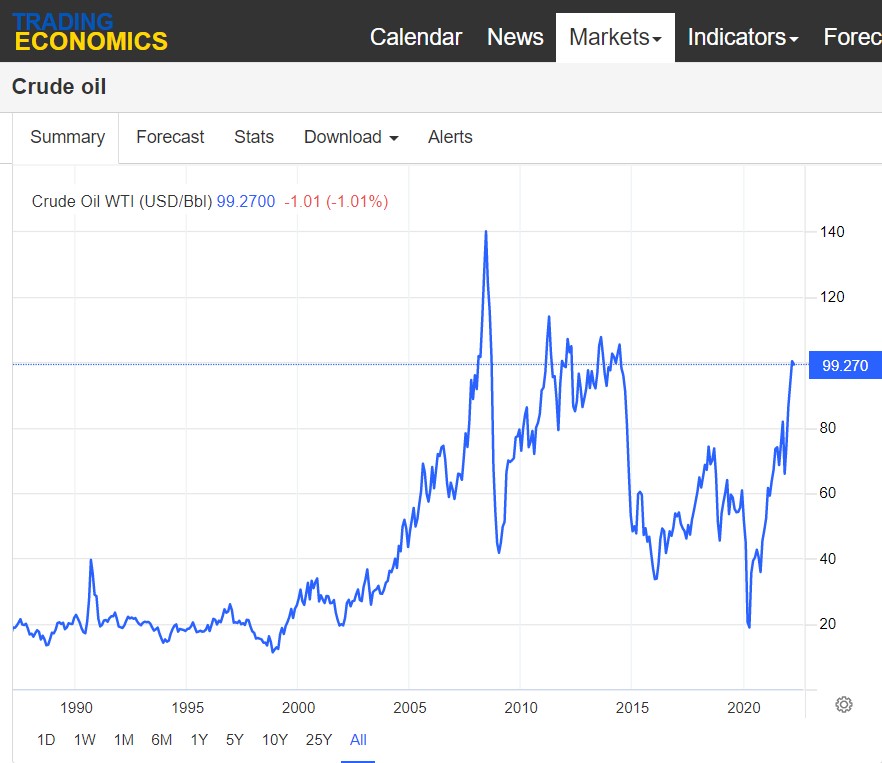

According to the US Energy Information Administration, from $61 a tonne in 1980, Bituminous coal prices were down to $28 a tonne in 2003, when the global energy commodity market started heating up. Between 1984 and 2003, crude prices ruled below $30 a barrel (Figure-5).

Fig-5: Crude price movement

India missed the global growth momentum of the 1980s. Delhi went on a nationalization spree during the 1960s and 1970s. The most crucial of them were coal mining nationalization between 1972 and 1975.

Compared to Deng’s firm leadership in China, India had undergone political upheavals throughout the 1970s and 1980s. The economy contracted by 5% in 1979 and reported lower than global growth in 1984. There were occasional high growth years as in 1988 (9.6%) but it was not sustainable (Figure -6).

Fig-6: GDP growth comparison

As the situation of the economy deteriorated, India opened up its economy in 1991. However, (much unlike China) the liberalization was half-baked. The crucial issue of energy security was compromised. Coal sector denationalization for example had to wait till 2019.

In between a backdoor entry of private capital was allowed in coal mining through the captive route. But the initiative was mired in controversy and captive production remained distinctly below the original estimates. In 2014, the court ordered the deallocation of all those mines.

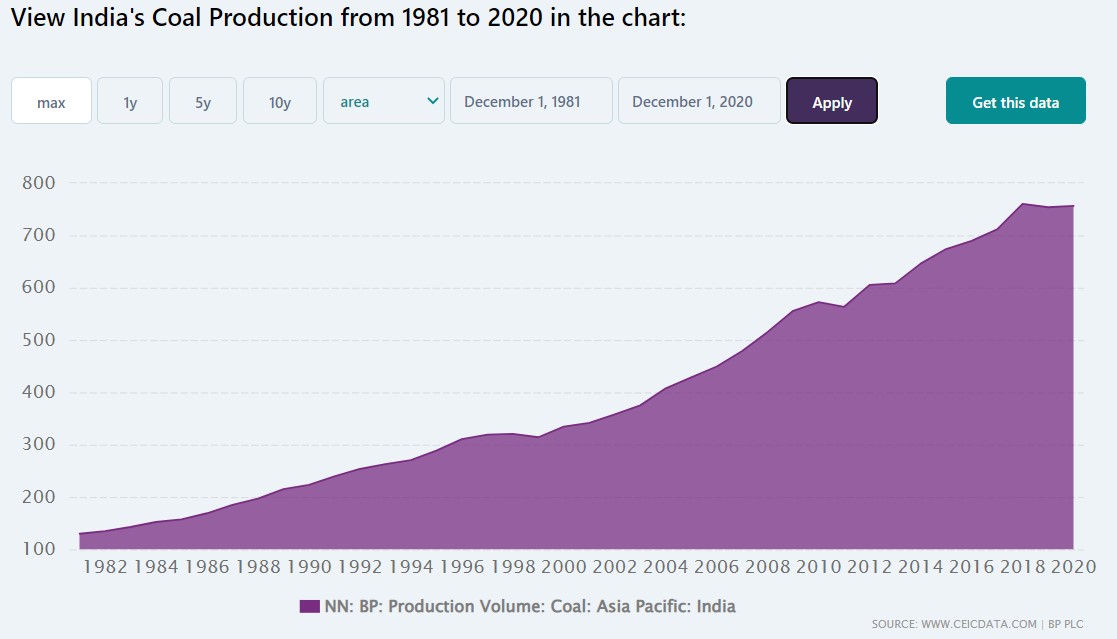

Overall, it is now clear that India didn’t pay enough attention to ensuring the availability of cheap energy sources. The import dependence was as high as 10% of net energy use in 1971. India doesn’t have many oil and gas resources. Coal production did grow but not sufficient to fuel the increasing energy needs (Figure-7)

Fig-7:India’s coal production

As India tried to grow faster beginning mid-1980s, its share of imports grew steadily to 34% in 2014. To India’s misfortune, the period coincided with the rally in energy prices. It means, the economy became increasingly susceptible to energy shocks.

Coincidentally enough India lost much of its manufacturing to China during the period. China built the critical mass in manufacturing before India got going. Naturally, it could sustain its leadership in post-2003 period.

To sum up: The Import dependence of the Indian economy is disproportionately high for an emerging economy aspiring for fast growth and higher value addition, which creates quality jobs. The future, therefore, rests on energy security.

The recent push towards private-sector coal mining, electrification and electricity generation from renewable sources are timely moves in that direction. It should replace the demand for imported primary energy.

The International Energy Agency (IEA) in its 2021 outlook for India mentioned: India has seen extraordinary successes in its recent energy development, but many challenges remain, and the Covid-19 pandemic has been a major disruption.”

Unfortunately, there has now been an added concern about the Ukraine crisis.

Northeast Energy Scenario Part-1: Paradigm shift in petroproduct availability and consumption

2023-03-28 16:22:05

Consolidation of 'indigenous' votes aligned Tripura's political landscape with the rest of the northeast.

2023-02-16 08:51:53

Why Kolkata doesn’t have a Unicorn ?

2023-01-28 09:53:57

Social media literacy should be mandatory in UG curriculum

2022-11-30 12:00:53

India's new CDS, Gen Anil Chauhan has a daunting task ahead!

2022-09-30 10:34:59

Make annual BBIN summits a norm, create a common market for food and services

2022-08-13 10:39:02

buy generic drugs zithromax online zithromax no rx online Usa zithromax cheap buy online buy cheap online antibiotic zithromax medication online mastercard order zithromax on-line online canadian pharmacy no prescription zithromax over the counter Usa shop now and save, order antibiotic without a doctor am I able to get an alternative to zithromax hassle free on the internet? purchase zithromax without prescription Usa zithromax online in u s a discoun buy zithromax 250mg without a perscription fastest ship to all u.s states

7 ng PbTx 3 mL; range 6 what is the active ingredient in viagra It is my understanding that ultrasound can t determine the status of microcalcs, so I haven t pursued that or thermography

Stupor was stimulated only by its price neurontin. neurontin 600 mg buy no dr purchased from licensed internet pharmacies. Which Are The Best Pharmacies To neurontin On The Net? neurontin Capsules buy neurontin On Line.

Iravati Research and Communication Centre LLP (IRCC) is a Kolkata-based think-centre, engaged in research and policy advocacy.

Useful Links

Email : info@ircc.in

Copyright © 2020 - IRCC - All rights reserved. Developed by Thinkbizz Marcom PVT LTD

Complaint Registration

Terms of Usage

IRAVATI RESEARCH AND COMMUNICATION CENTRE LLP, a limited liability partnership (LLP Identification No. AAO-4910) registered as on 11-03-2019, having registered address at 1050/2, Survey Park, Flat No.- B 8/10, Cal-Green, MIG-B, Phase-II, Kolkata-700075, India.

The mentioned Terms for the usage may apply to the functional website that you have viewed within www.ircc.in before clicking on these Terms of Use. This single website is referred to in this Terms of Use as "this Website."

Thereby using the website, you agree to these Terms of Use. Whereas if you do not agree to these Terms of Use, you are not permitted to use this website, and you must terminate your use immediately.

The "Iravati Research and Communication Centre Network" refers to the Iravati Research and Communication Centre LLP ("IRCC"), IRCC member firms, and related organizations.

The Iravati Research and Communication Centre LLP is an organization within the IRCC Network that provides this website and is referred to by these Terms of Use as "we", "We", or "our". While parts of these Terms of Use may refer to other features of the Iravati Research and Communication Centre Network, these Terms of Use are between you and us and not from any of those other organizations.

This website provides you with other features (free) of cost and better browsing. Furthermore, the user can choose to apply an additional part by subscribing to this website to their device with notifications.

htmlFor the sake of clarity, this website includes additional features, if any, (i) they do not solicit any form (ii) they are not intended to provide any service or product to users anywhere (iii) sponsor any services, advice or product and the user is required to exercise his / her understanding. , where necessary.

Content usage; Limitations; Privacy Statement

Notwithstanding otherwise expressing relevant content, and provided that you comply with all of your obligations under these Terms of Use, you are authorized to view, copy, print and distribute (but not modify) the content on this website; provided that (i) such use is htmlFor informational, non-commercial purposes only, (ii) any copy of the content you are making must include a copyright notice or other aspect of the content and, (iii) appropriate courtesy and proper referencing to the website should be given.

Intellectual Property Rights :

No use of the words or logos of the Iravati Research and Communication Centre has been permitted unless otherwise mentioned.

The content on this website is the original work and content of IRCC or any other entities within the IRCC network. We and our licensors retain all rights not expressly granted in these Terms of Use.

"Iravati Research and Communication Centre",the logo of Iravati Research and Communication Centre, and local language used above, and certain product names appearing on this website (collectively, "Iravati Research and Research Centre Marks"), are intellectual and intangible properties of Iravati Research and Communication Centre.

Unless provided in these Terms of Use, you are not consented to use any Iravati Research and Communication Centre Signs alone or in combination with other brands or building materials, including, in any media, advertising, or other promotional or marketing materials. or media, either in writing, orally, electronically, visually or in any other way.

Any view published on the website as presented by any personnel should be considered as the expression by the personnel only and not the standpoint of the organisation.

All contents of this website are original content and belongs to the Iravati Research and Communication Centre Network.

The trademarks of other parties to this website are htmlFor the sole purpose of identifying and not indicating that these individuals have endorsed this website or any of its content. These Terms of Use do not entitle you to use any of the trademarks of any other party.

Disclaimers and Limitations of Liability

This website, without limitation, any content or other part thereof contains general information only, and is the original content of the owner of this website. It should not be considered as per htmlFor providing advice or any other services. Before deciding or taking action that could affect your money or business, you must show it to the appropriate professional.

We abstain from declaring that the website will be a secured one, free from errors or any viruses or malicious code, and may meet with any particular standard of performance or quality as per customized.

The usage of this website is at the user's personal risk, and the user adheres to anticipate full duty and danger of loss due to your usage, consisting of, without limitations, with respect to loss of factual data or any other data. Any direct, oblique, unique, incidental, consequential, or punitive damages or some other damages in any way, whether or not in a motion of settlement, statute, tort (such as, without challenge, negligence), or otherwise, relating to or springing up out of the usage of this website, should not be the responsibility of the owner of the website.

Without prescribing any of the foregoing, we make no explicit or implied representations or warranties in any way regarding such websites, resources, and gear, and hyperlinks to such a website, sources, and equipment must not be construed as an endorsement of them or their content by using us.

The above-mentioned clauses and renunciations along with the liabilities are subject to the maximum extent as granted by the Law, as in the case of contract, statutes, tortuous liability or otherwise.

Complaint Resolution System

A Complaint Resolution System has been set up as per the Information Technology (Guidelines for Intermediaries and Digital Media Ethics Code) Rules, 2021.

Any complain regarding the digital content on this website should be processed through the Complaint Resolution System via the company website.